NPS is an easily accessible, low cost, tax-efficient, flexible and portable retirement savings account. Under NPS, the individual contributes to his retirement account and his employer can also co- contribute for the social security/welfare of the individual.

Get a help

Introduction

Pension Fund Regulatory and Development Authority (PFRDA) was established in 2003 to promote old age income security

PFRDA launched the NPS Corporate Sector Model in December 2011 as an initiative to promote NPS for the employees working with Corporates

It facilitates employees working with various organizations to on board NPS within the purview of their employer – employee relationship.

As on 31 Mar 2024, count of NPS subscribers was 1.85 crores out of which 16.5 Lacs are from corporate sector

Operated through single PRAN*

All Citizen Model

An individual can open NPS account, & voluntarily contribute towards his NPS to build his pension corpus

It is popularly also known as Individual or Retail model

This model is available since 2009

Corporate Sector Model

This is a separate model to provide NPS to the employees of corporate entities, including PSUs to additionally contribute to their own NPS account through their Corporate*

This model was launched in 2011

Permanent Retirement Account Number

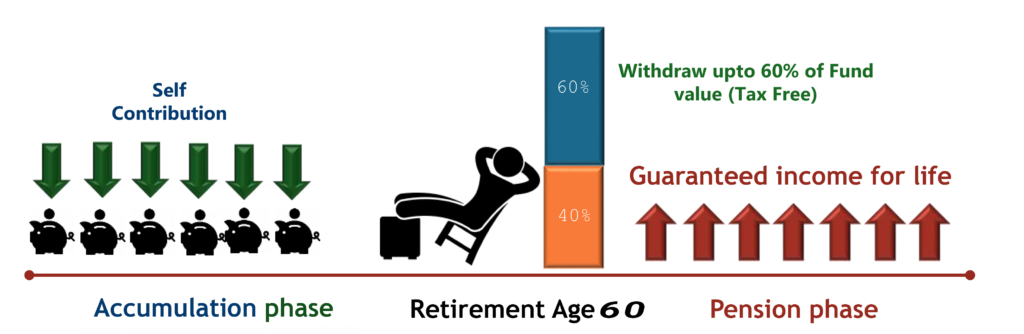

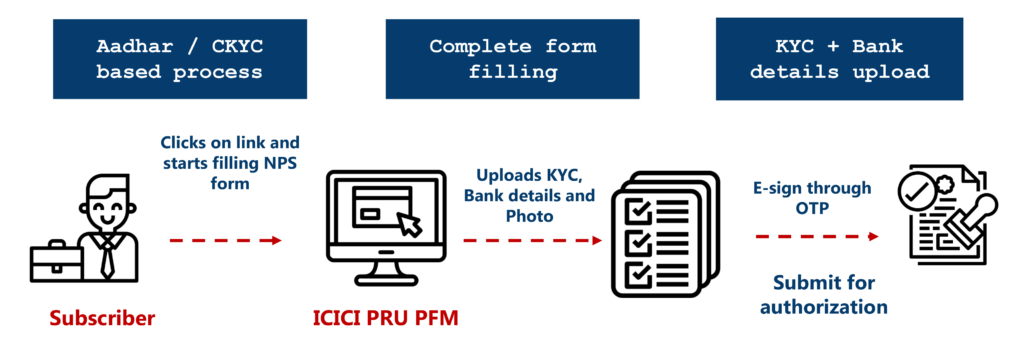

How Retail NPS works

Individual regularly invests in NPS account

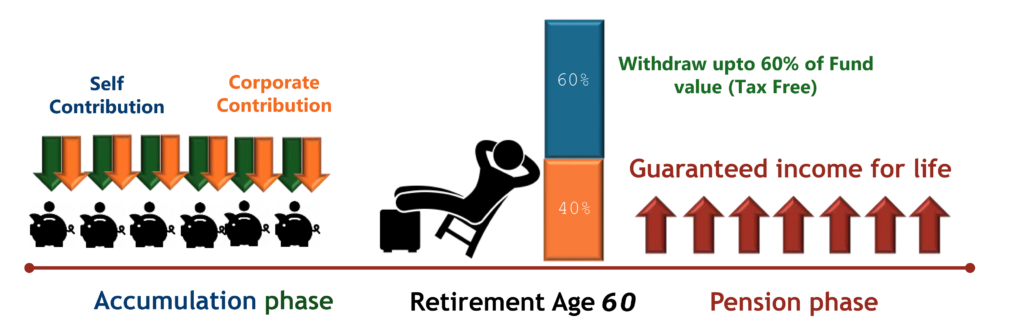

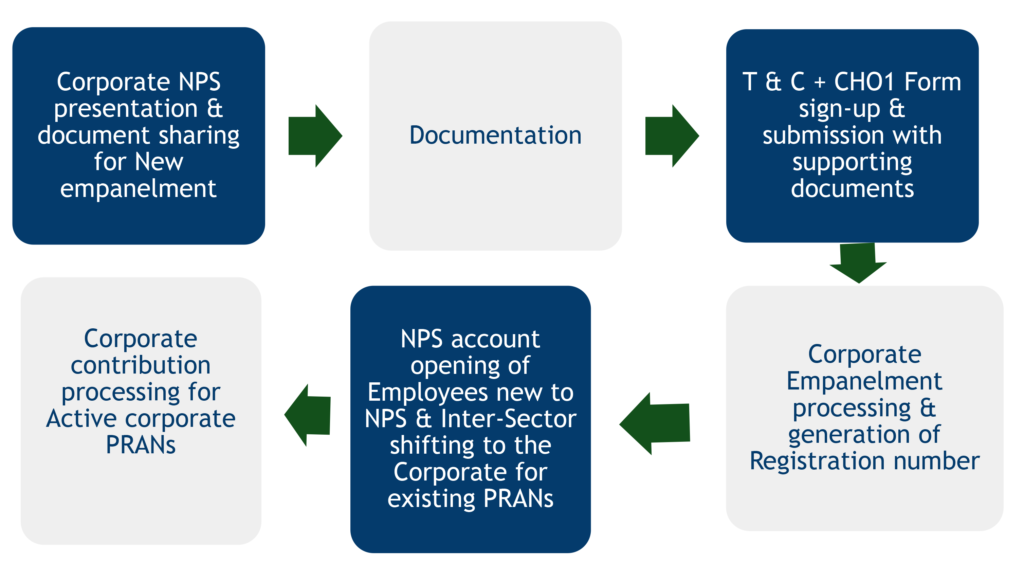

How corporate NPS works

Corporate contributes regularly. Employee may also contribute in same PRAN

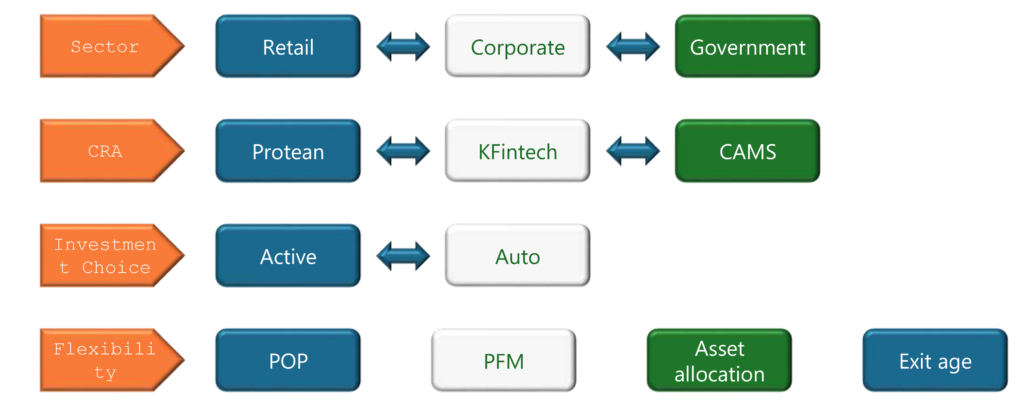

NPS: Key constituents

Point of Presence Acts as first point of interaction for subscriber Responsible for account opening, receiving contributions and instructions from subscribers

NPS Trust Responsible for taking care of the funds under NPS by prudently monitoring / auditing portfolio of Pension Fund Manager on regular basis

Annuity Service Provider Responsible for providing Annuity Service after Subscriber exits from NPS

Pension Fund Manager: To be responsible for managing the retirement savings of subscribers under NPS

Central Recordkeeping Agency: Responsible for recordkeeping, administration and customer service functions for all subscribers of NPS

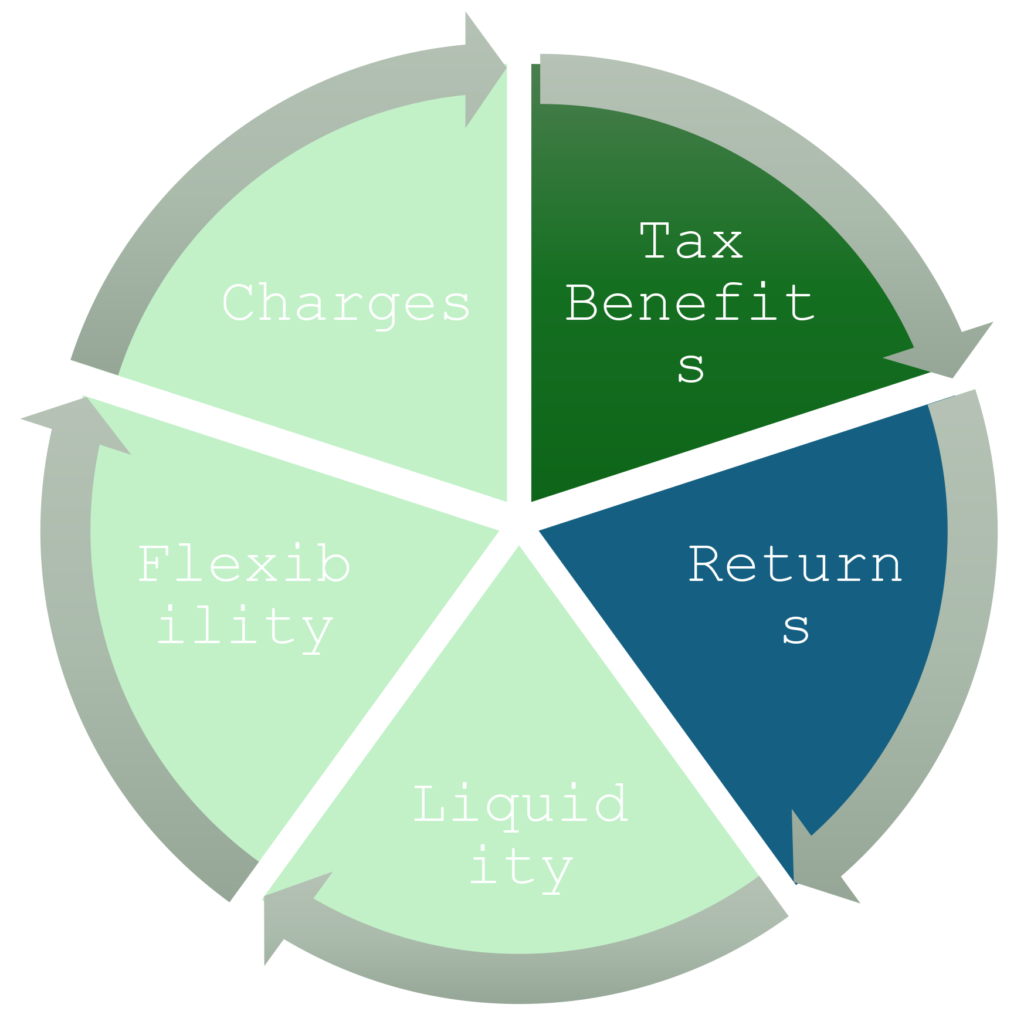

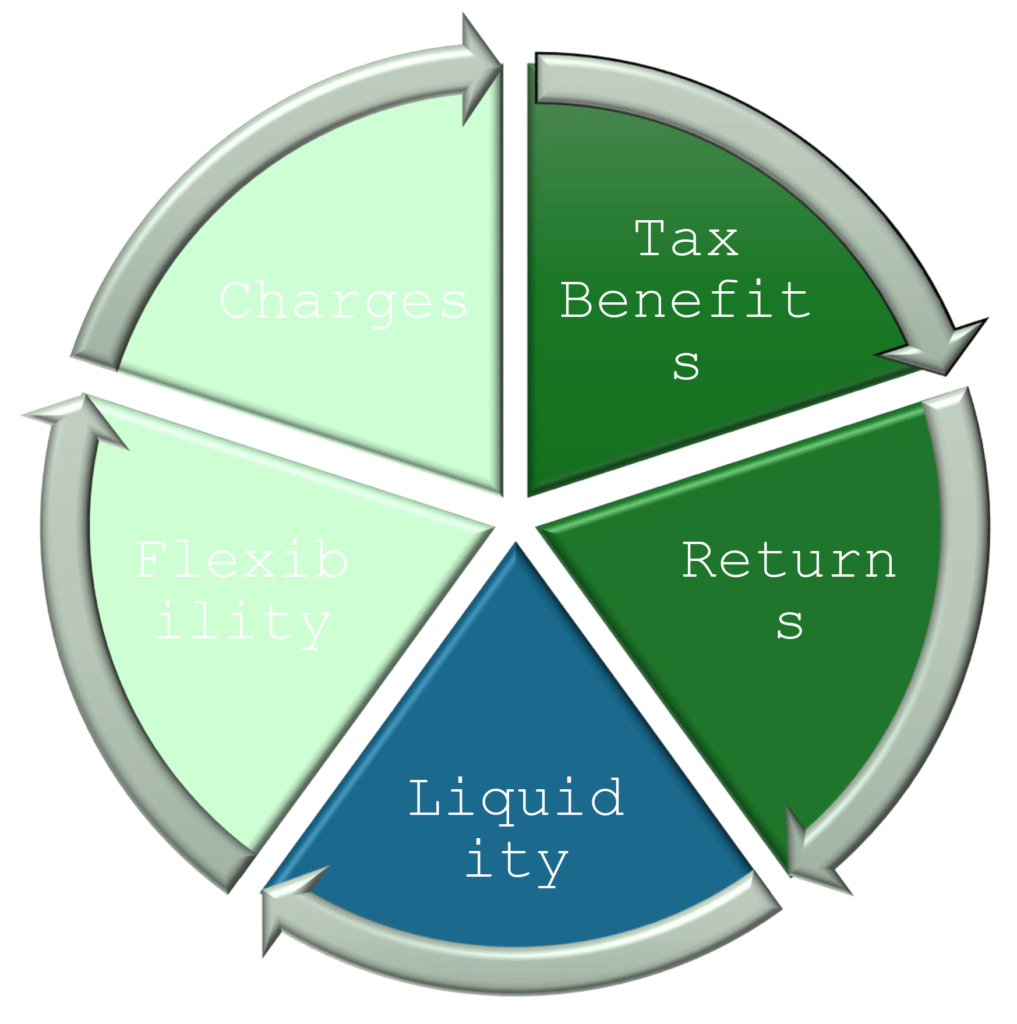

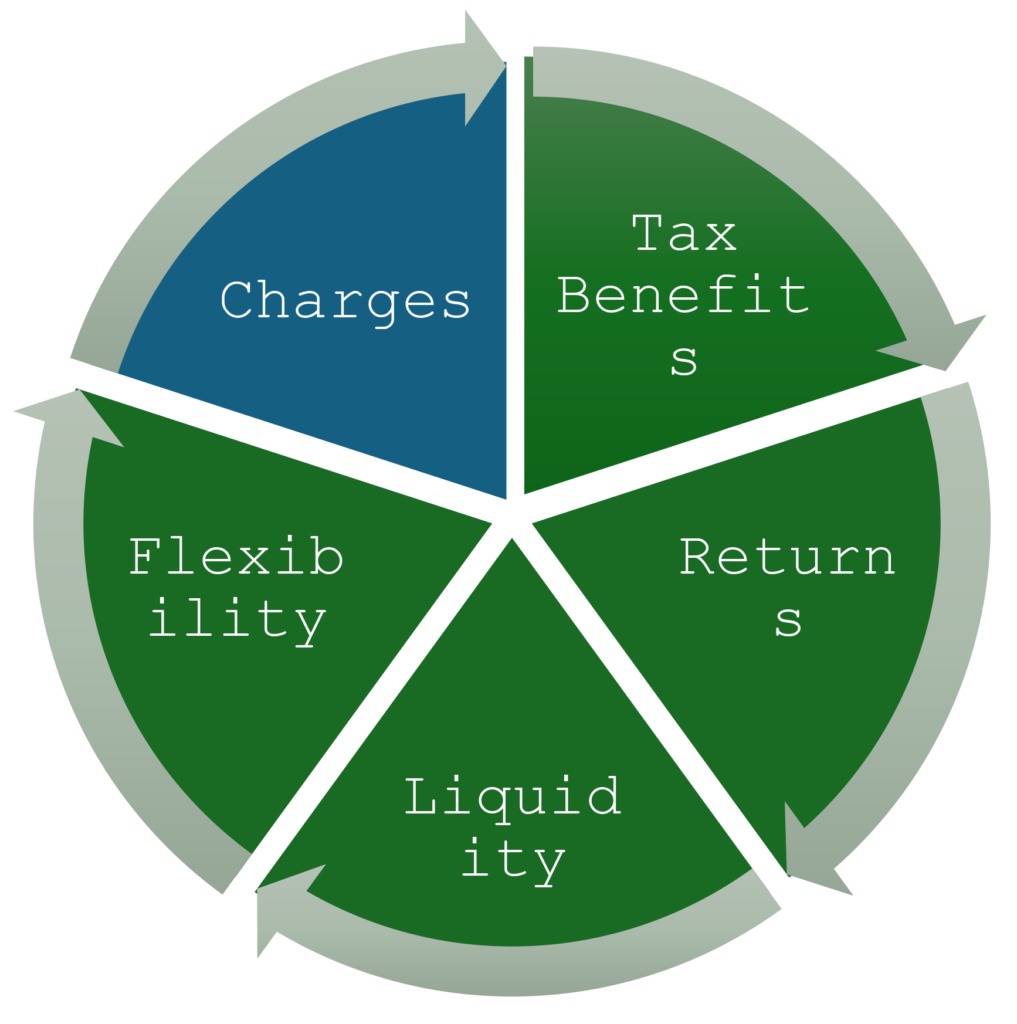

NPS features & benefits

Portable

Carry your account across employers, location etc.

Simple

Standard product regulated by PFRDA

Flexible

Choose your fund manager, investment option & annuity options

Economical

Lowest cost investment product currently available in the market

Corporate contributes regularly. Employee may also contribute in same PRAN

Flexibility

NPS features & benefits

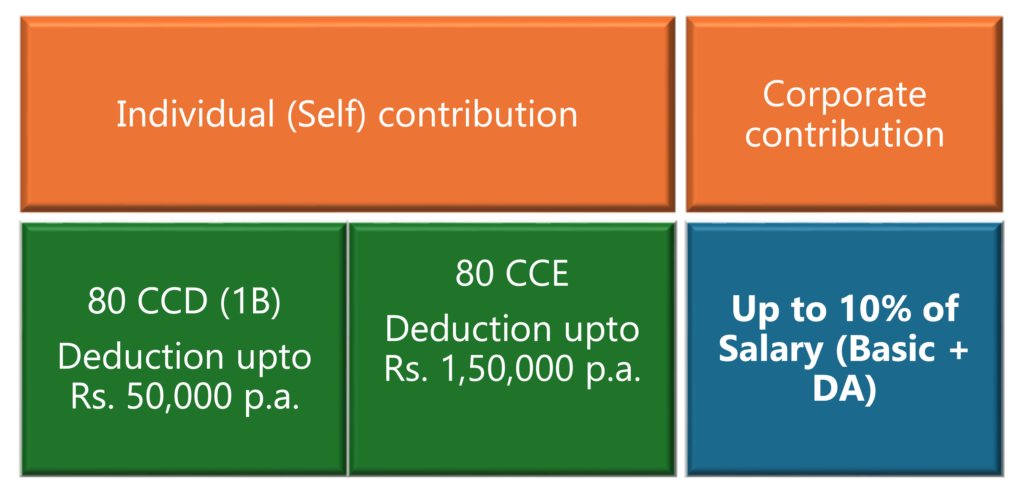

Tax Benefits

Multiple tax benefits

Capping of 7.5L on contribution towards (NPS + SA+ PF)

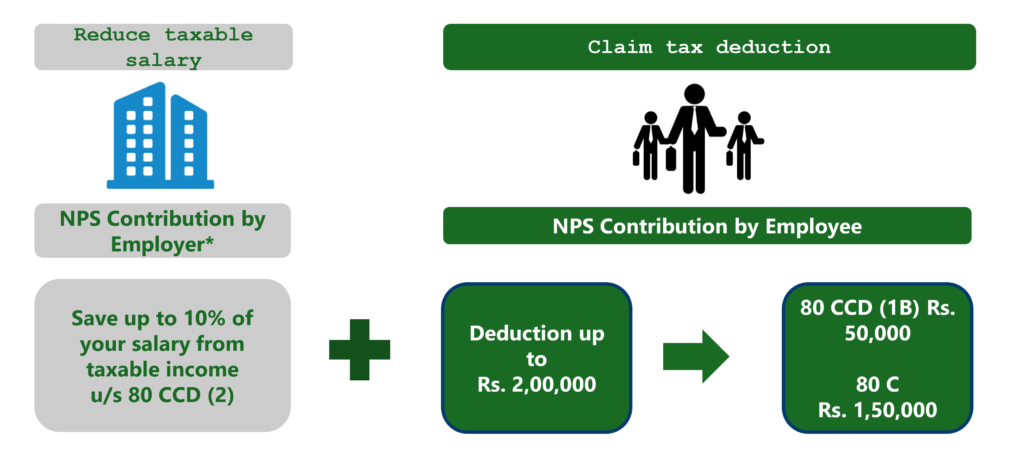

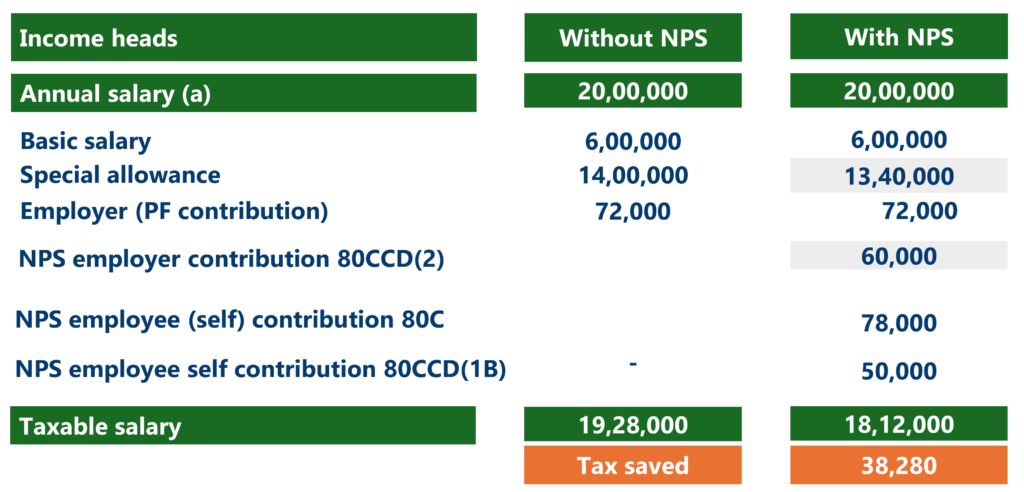

Sample illustration – Reduce taxable salary

NPS features & benefits

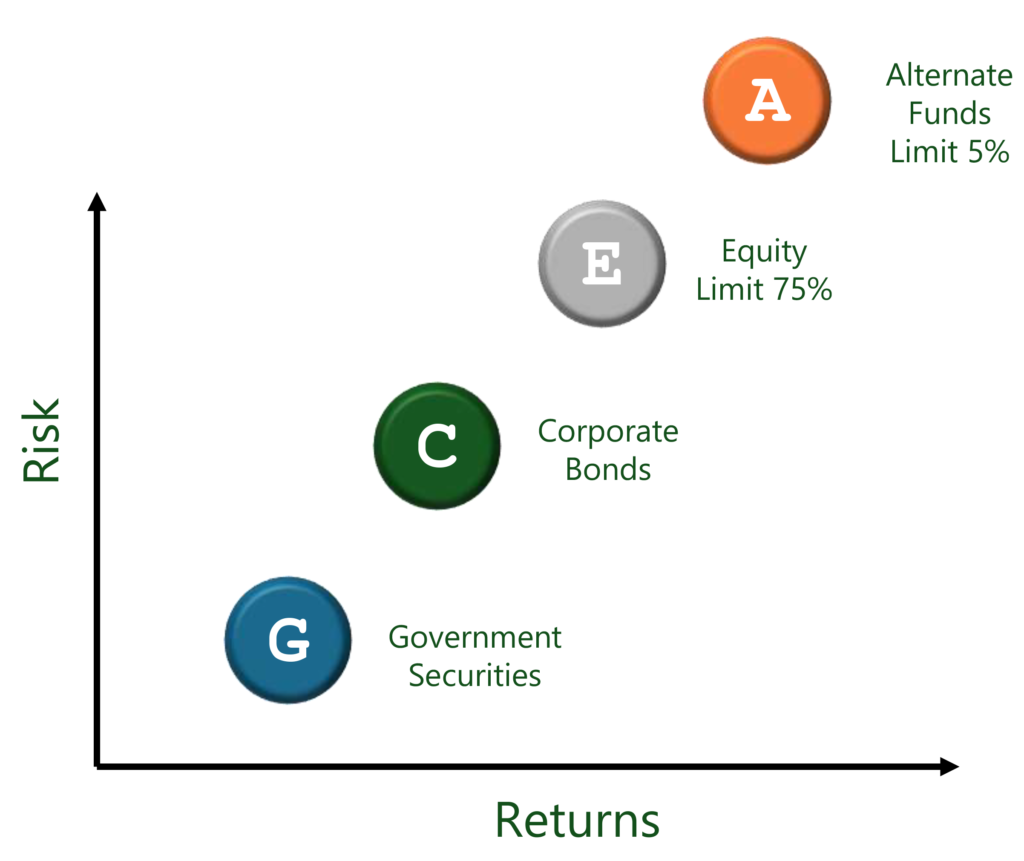

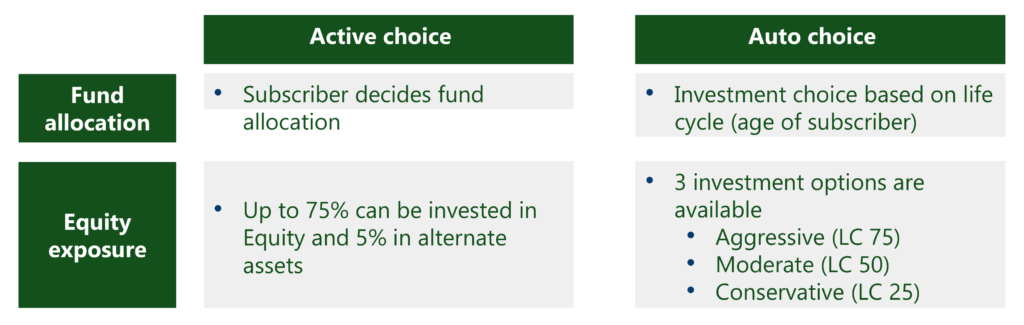

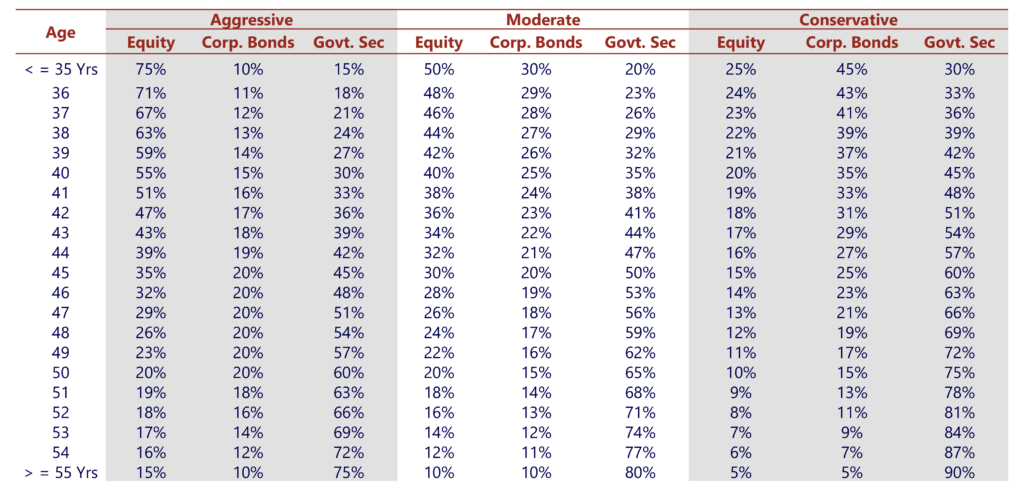

Fund options under NPS

Investment choices

Auto allocation

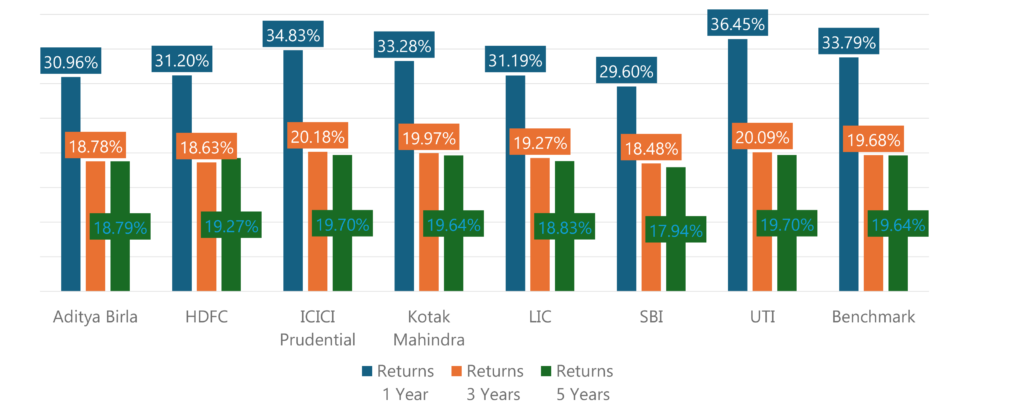

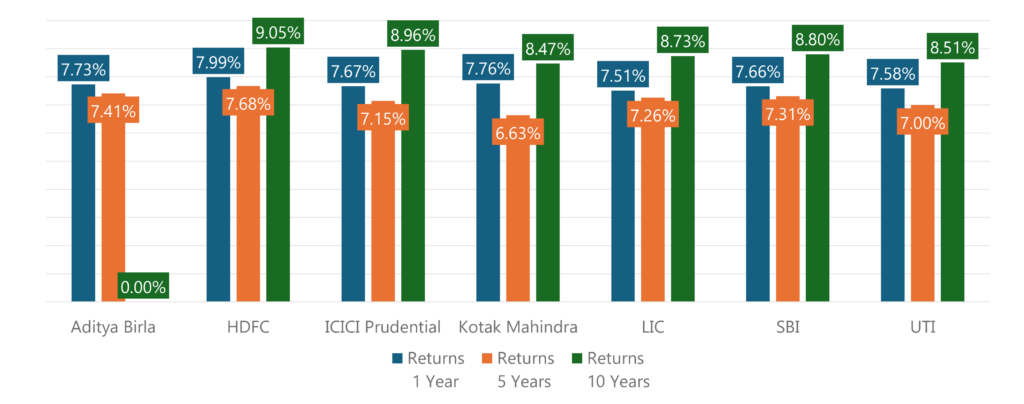

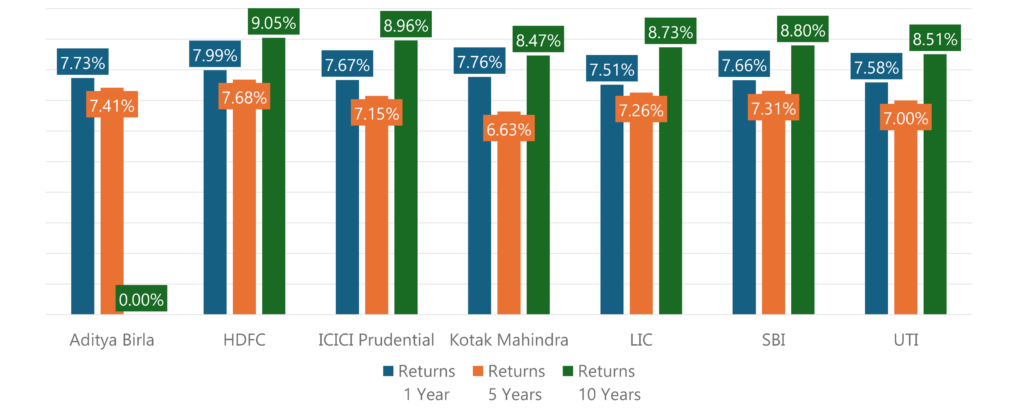

NPS Returns: Fund E

As at 19 July 2024 * NPS Trust

NPS Returns: Fund C

As at 19 July 2024 * NPS Trust

NPS Returns: Fund G

As at 19 July 2024 * NPS Trust

NPS features & benefits

Partial Withdrawal

Subscriber can now withdraw 3 times from NPS corpus after completing 3 years in the system.

Subscriber can withdraw 25% of contribution made by them; excluding contribution made by employer & growth generated, adhering to below condition

Education of self & children

Marriage of children

Due to critical illness of self / spouse / children

Construction / purchase of residential property

Exit from NPS

Vesting criteria

Benefits

Upon normal superannuation

(60 year)

Min 40% of the NPS corpus should be annuitized.

Max 60% is paid as lump sum to the subscriber.

If the corpus is less than Rs 5 Lacs then full withdrawal is permitted.

Exit from NPS before the age of normal superannuation (e.g.

Voluntary Retirement)

Allowed after 5 years of NPS account opening

Min 80% of the NPS corpus should be annuitized

Max 20% is paid as a lump sum to the subscriber and it is tax free

If the corpus is less than Rs 2.5 Lacs then full withdrawal is permitted.

Upon death

NPS corpus (100%) paid to the nominee/ legal heir of the subscriber. The nominee can choose to take the annuity as well

Continue your NPS account

You can be in NPS till 75 years of age and continue to avail tax benefits

NPS allows Subscriber an exclusive Tax Benefit upto Rs. 50,000 u/s 80CCD(1B) over and above the limit of Rs. 1.50 Lakh u/s 80C

You will continue to enjoy all the facilities and options of normal NPS account like option to switch fund managers and assets class etc. during the continuation period.

Vesting criteria

You can defer your Withdrawal and stay invested in NPS up to 75 years of age.

Multiple deferment options available.

Defer only Lump sum withdrawal

Defer only Annuity

You have an option to withdraw deferred lump sum amount in a phased manner over a period of 10 years or withdraw entire amount anytime.

NPS features & benefits

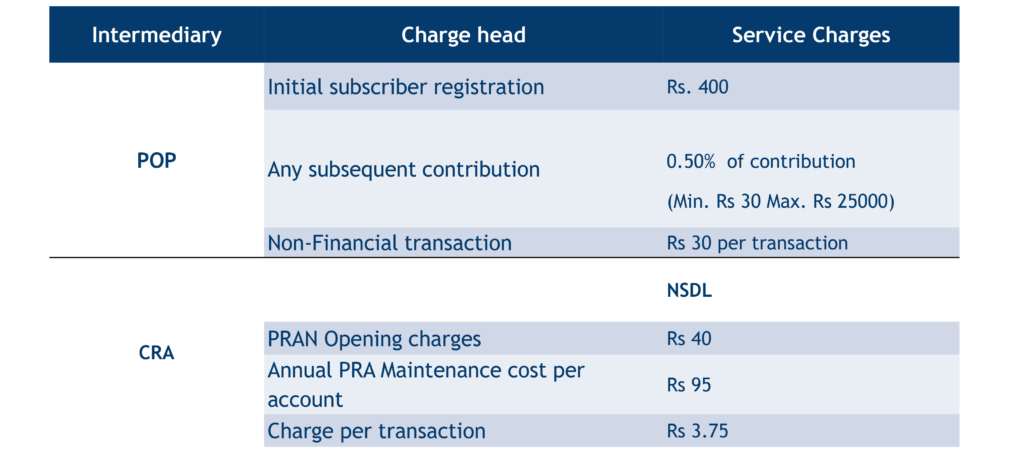

National Pension System Charges

Corporate NPS benefits

Retail NPS

No authorization required by corporate

Normal exit at age 60

Exit request is authorized by POP

Subscriber has freedom to select annuity service provider and option

Retail NPS

NPS Exit

Corporate NPS

Corporate has to authorize new subscriber (online) through corporate login

Normal exit at age of superannuation

POP authorizes exit request after confirmation from corporate

Subscriber has freedom to select annuity service provider and option